Dear investor,

The reason for writing a letter to our investors is to summarize our investment performance. In our ideal world, this letter would be written every five years, as this is our minimum investment horizon. However we believe that our co-investors should have all the necessary information to assess the job we do. It is in this spirit that we address these quarterly missives.

The results obtained by our funds are reflected in the table below. The individual return of each investor depends on the net asset value at which they subscribed:

With respect to our previous quarterly letter, Azvalor Iberia increases the difference relative to the index up to more than 8 percentage points so far this year. In the case of Azvalor Internacional, the fund has recovered more sharply: we have gone from losing 2% relative to the index at the end of January, to obtaining over 12% at the end of April (MSCI World).

International Portfolio

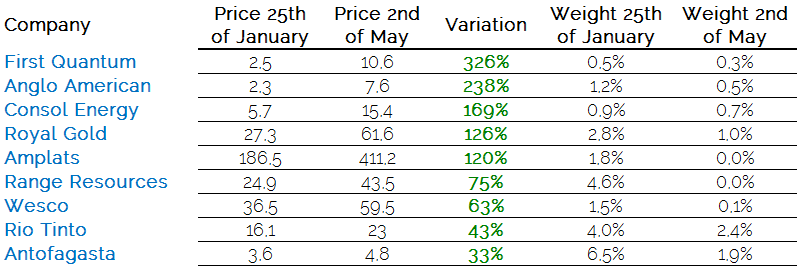

A significant part of our portfolio has achieved in only three months the returns we expected to reach in a period of five years. As always in such cases, when the market recognises the value, we seize the moment to reduce positions, in some cases completely. The exposure to commodities has approximately halved.

There is another part of the portfolio which hasn’t performed so well. Once again, what we usually do in these cases is strengthen the position, if nothing has changed in the investment thesis. Marie Brizzard or Financière de l’Odet are two examples of such cases. We have also incorporated over 15 new companies (Zodiac, Devon, Cabot Oil & Gas, Weir, Panalpina, Richemont, etc.). In general, these are good businesses with healthy balance sheets which for some reason (in our opinion, temporary) have been punished in the stock market. We prefer not to give too much information about them to avoid possible damages to our trading operations.

Iberian Portfolio

Perhaps what has been most sticking is the sale of the position in Arcelor Mittal. The reason was threefold: its shares rose by over 50%, its target price was reduced by over 25% as a result of the capital increase, and some investment alternatives fell by 25% during this period. This made it considerably less attractive compared to other possible opportunities, namely:

- Técnicas Reunidas: After the profit warning issued by the company in mid-February, we substantially increased our position, at a price which values recurring profits we estimate at less than 7x. Such price level, the strength of the balance sheet, and owners-managers we especially admire, provide the necessary comfort to accompany them throughout this toughest part of the journey.

- Mapfre: We have considerably raised the weight, at a price which values at zero the majority of its international business. We do not think that the understanding of banking problems can be “automatically” extended to Mapfre, nor that Life is a high-risk business segment, as assets and liabilities match up. Although it is true that some typical exposures of insurance companies could represent a challenge in the event of a financial crisis (slump in bonds and rest of markets), Mapfre would be no worse than other insurance companies, but nevertheless it trades at a very high discount compared to them.

Current attractiveness of our investments

Between the summer of 1998 and March 2000, a part of the market (the “dotcoms”) was trading at stratospheric multiples, while most of the “old economy” companies languished, trading at one-digit multiples. The majority of those who invested in dotcoms lost everything in a couple of years, while the rest of the stock market didn’t do so badly. We see some parallelisms (without exaggerating!) with this period today:

- In our opinion, bonds are a bubble, many of them trading with negative IRR, and we believe they will be loss-making for their current holders.

- Whatever is a “substitute” of bonds (stable, defensive shares) has had some artificial buying pressure since QEs were launched some years ago. These shares also scare us.

- However, we still find low-priced shares, and some rare cases of inexplicable undervaluation. For instance, Hyundai’s preference shares value the company in 26 trillion KRW, and the net cash and investments not subject to the business alone add up to 29 trillion KRW = they “pay” us 3 trillion KRW (approximately 3 billion USD!) for being the owners of a company that produces 5 million cars with an EBIT margin of 7%.

It is in this dichotomy of valuations between financial assets that we see the parallelism with the period of the dotcom bubble. Then, the best strategy a posteriori would have been to run away from expensive shares, finding refuge in the cheap ones (indices dropped and these investments appreciated). Our recommendation, as always, is to be invested.

Many investors ask us in what percentage they must do so. Our advice is: that quantity which, in the light of one’s own personal circumstances, will not be needed in the next 4-5 years. This is the only way to avoid the temptation of selling amidst a possible sharp fall in the markets.

Azvalor Iberia has businesses with an average ROCE of 17% which are worth 50% more; this potential stands at 70% in the case of Azvalor Internacional, with an average ROCE of 29%. Moreover, both funds have an ample liquidity position, after the sales made with the rise in commodities, destined for a list of very interesting companies, in the final stage of study. Our model portfolio continues to have an exposure of 80% Azvalor Internacional / 20% AzvalorIberia.

Azvalor news

Azvalor continues its frenetic activity:

In the analysis department, we have held 330 meetings/conferences with companies, competitors, suppliers or sectoral experts since 1st February. The result is a list of new investments and a very interesting degree of progress in many others.

In the investor relations department, we have answered calls and received visits of investors, who already number more than 3,500. To this day, we manage 851 million euros in institutional mandates and 639 million euros in investment funds.

The people who make up the funds’ administration, the back-office and the trading desk continue to respond magnificently to work, as a result of which we have finally been able to reduce the minimum amount required to invest in our funds, which can already be subscribed for €5.000. We hope to be able to announce shortly that we have a vehicle to manage pension funds, although the date is still uncertain.

We would like to thank you for the trust you have placed in our management and your support at all times. The investor relations team, led by Beltrán Parages, will be pleased to answer any questions you may have.

Álvaro Guzmán de Lázaro Mateos

Chief Investment Officer