Dear investor,

The underlying reason for writing a letter to our investors is to illustrate the results obtained. In our ideal world, this letter would be written every five years, as this is our minimum investment horizon. However, we believe that our co-investors should have all the necessary information to judge our work. It is in this spirit that we have addressed these quarterly missives since our inception.

The results obtained by our funds in the first quarter of this year are reflected in the table below. The individual return of each investor depends on the net asset value at which they subscribed:

| Jan-Mar | Jan-Mar | |||

| Azvalor Internacional FI | 4.6% | Azvalor Iberia FI | 5.7% | |

| MSCI Daily Net TR Europe Euro | 6.0% | IGBM Total** | 12.5% | |

| Return vs. Index | -1.3% | Return vs. Index | -6.8% | |

| MSCI World | 5.9% | IGBM | 11.8% | |

| Return vs. Index | -1.2% | Return vs. Index | -6.1% | |

| ** Includes dividends | ||||

| 85% IGTBM / 15% PSI 20 TR | 11.7% | |||

| Return vs. Index | -6.0% |

The first quarter of the year has closed with positive absolute returns (we have made money) although below the benchmarks (i.e. others have made more than us).

Should we invest in indexes now that they are doing so well?

We analyse this phenomenon in detail trying to answer the following questions:

- To what extent do indexes outperform fund managers?

- How long does the greater return of passive products usually last?

- Is it convenient to invest in them?

- Does the current outperformance of passive management mark a “new era” or alert us about overvalued markets?

The table below shows how an investor would have nearly always achieved greater return in passive products than in the average of the funds marketed in Europe. Hence, only 9% of European stock funds have managed to outperform the benchmarks over a 10-year period.

Table 1. Percentage of funds sold in Europe with lower returns than their benchmarks

| Category | 3 years | 5 years | 10 years |

| Global | 89% | 96% | 98% |

| USA | 93% | 97% | 99% |

| Eurozone | 85% | 88% | 91% |

| Emerging | 82% | 89% | 97% |

Source: S&P Dow Jones LLC, Morningstar. Data for periods ending on 31Dec15.

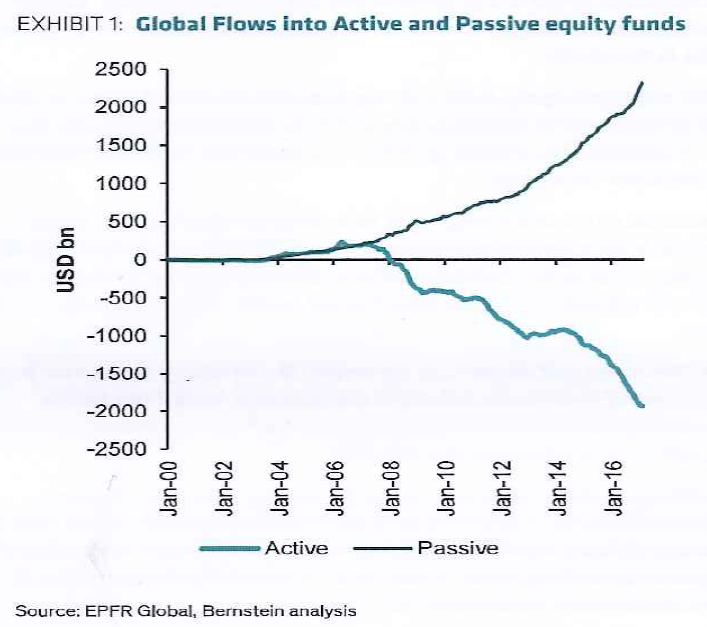

It seems that only a few fund managers actually outperform their benchmarks after expenses and, therefore, passively managed products would have a well-deserved place in the portfolios of the average client. This might explain the decline of active management over the past 8 years, as shown in Exhibit 1.

However, when a trend is widely accepted as permanent, our reaction is usually to address it with certain scepticism and get down to work in order to understand it better. As always, we turn to history first:

- Have indexes ravaged active managers in the past?

- What were the consequences?

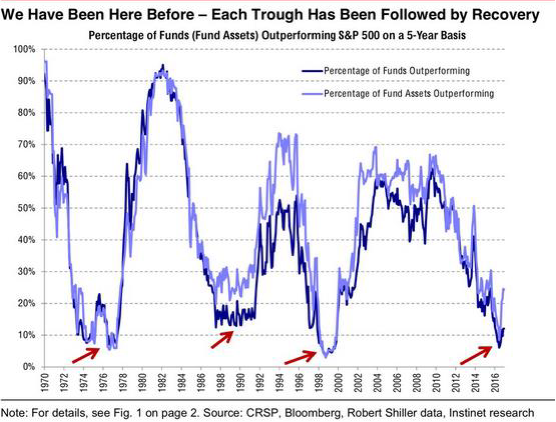

Now, look closely at the following graph. It shows:

1) that this moment is one of the 4 periods in the past 50 years in which benchmarks have outperformed active managers,

2) that historically this phenomenon, so sharply articulated, does not usually last long,

3) that indexes collapsed when current levels were historically reached; the last one that Fernando and I witnessed was in 1999 (see the arrow on the graph); and although the market (the indexes!) started to fall in March 2000, this did not prevent most active managers like us from generating excellent returns that same year.

Graph 1. Percentage of Funds Outperforming S&P on a 5-Year Basis

Although it seems that we are not dealing with a “new paradigm”, perhaps the last “test” of a bubble is to detect situations that defy common sense.

Just like tulips were sold for fortunes in the 17th century, or “dotcom” companies without any sales or clients were easily worth hundreds of millions on the stock market in the late nineties, today we have detected some situations with regard to passive products which defy common sense.

For instance, as shown in the two tables below, the “irony” lies in the fact the investor who buys a passive product (ETF) to bet on Spain… (notice the composition of the index)

| ETF “Spain” Ishares MSCI Spain Index ETF | ||||

| weight | ||||

| Banco Santander SA | 13.1% | |||

| Telefónica SA | 9.0% | |||

| Banco Bilbao Vizcaya Argentaria | 7.6% | |||

| Iberdrola SA | 7.1% | |||

| Industria De Diseño Textil Inditex | 6.8% | |||

| Amadeus IT Holding SA | 4.9% | |||

| Repsol SA | 4.8% | |||

| Red Eléctrica Corporación SA | 3.8% | |||

| Aena SA | 3.6% | |||

| Ferrovial SA | 3.5% | |||

| Weight of 10 Largest Holdings | 64.3% | |||

… is not exactly betting on Spain! (notice the proportion of “Spanish” sales of the index members).

| % of sales OUTSIDE Spain | ||||

| Banco Santander SA | 88.0% | |||

| Telefónica SA | 73.7% | |||

| Banco Bilbao Vizcaya Argentaria | 71.6% | |||

| Iberdrola SA | 55.0% | |||

| Industria De Diseño Textil Inditex | 82.3% | |||

| Amadeus IT Holding SA | 96.2% | |||

| Repsol SA | 47.6% | |||

| Red Eléctrica Corporación SA | 2.1% | |||

| Aena SA | 5.9% | |||

| Ferrovial SA | 72.2% | |||

Currently, there are some other signs contrary to common sense in the world of passive products, such as the fact that the investment vehicle is more liquid than the assets composing it. In times of market panic, this could lead to truly dramatic situations for the holders of said products.

Therefore, it seems that investing in indexes:

- Has proven successful in general, as they are cheaper than actively managed products, and there are very few managers outperforming them in the long term.

- At this particular time, we do not feel it is the best idea, in the light of historical data.

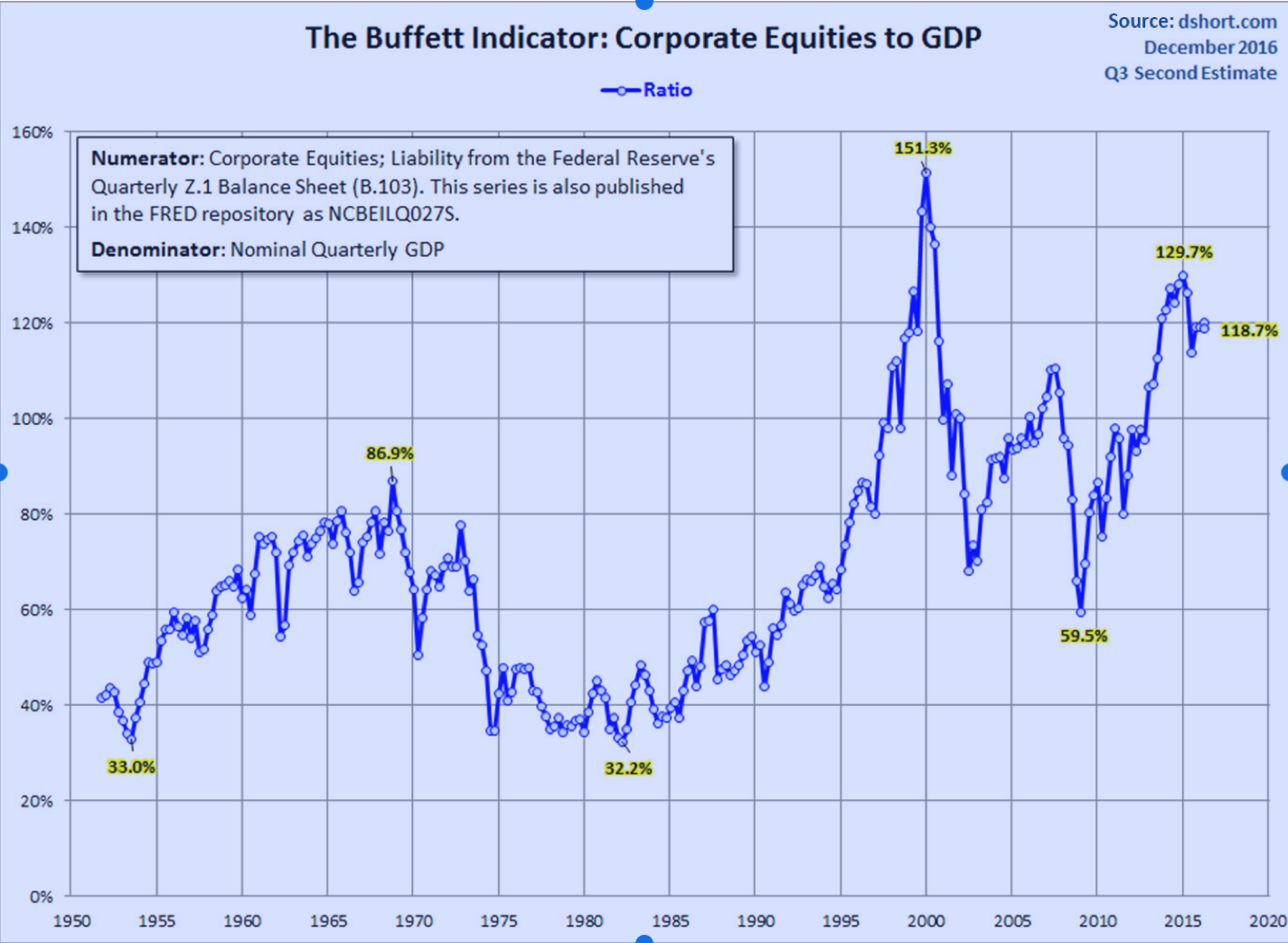

After all, investing in indexes is like betting (efficiently, of course, thanks to their low commissions) on equity markets continuing their upward trend. The graph below gives us a historical perspective of the current valuation levels compared to the past 70 years, using Warren Buffett’s favourite indicator.

This indicator (market capitalisation divided by GDP) is a very basic approximation to market valuation levels. As can be seen in the graph, late last year it was in the upper part of its historical valuation range, and after the return obtained this first quarter it is even more so now. This does not necessarily mean that the stock market will fall tomorrow, but knowing that companies trade at high multiples in relation to history gives us a certain perspective. We suppose that money creation by the Fed and artificially low interest rates have encouraged investment optimism, which explains why prices are relatively high.

In order to conclude the debate between active and passive management, we believe that today is probably the time when passive management is regarded worse than active management compared to the past 20 years.

If we do not invest in indexes, how do we make the right choice among active fund managers?

Even if we are right with our negative vision regarding index performance from current levels, it will continue to be true that only a minority of managers will manage to outperform them in the very long term. So, how can we find the members of this exclusive pantheon?

In Azvalor, the following quote pops into our mind:

“If you want to have a better performance than the crowd, you must do things differently from the crowd”. Sir John Templeton.

We do not think that doing things differently guarantees excellence, but doing them just like everybody else certainly ensures mediocrity. We believe that our “difference” in Azvalor has to do with more qualitative aspects of the investment arena, and while many may seem strange for the crowd, they are precisely what sets us apart from it. We summarise them below:

| Philosophy of the majority | Philosophy of Azvalor |

| Use stock brokers’ estimates | Own estimates |

| Risk=volatility | Risk=losing money |

| Returns relative to the index | Absolute returns |

| Trading mentality | Business owners |

| Diversification | Concentration |

| Macroeconomic predictions | Support in Austrian School to understand / no macroeconomic predictions |

| Culture of the majority | Culture of Azvalor |

| Local or global | Local and global |

| Accumulate assets | Limited capacity |

| Several types of assets | 100% Equities |

| Corporate governance is not a priority | Obsessed with corporate governance |

| Managers do not put their money at stake | Managers put most of their assets at stake in funds |

In addition, we believe that the concurrence of, at least, 3 fundamental elements is required in order to generate exceptional returns:

1) visions of the companies different to consensus, based on a more in-depth analysis of data, which in general end up occurring,

2) the conviction to maintain them in spite of the enormous pressure to give up and adapt to “the majority”, especially at times when one seems to be temporarily wrong (in Azvalor, this is what happened to us with commodities at the beginning of 2016),

3) humility to withdraw from an investment when you have made a mistake.

All of the above materialises in something where we place our greatest effort every day: our portfolios. We believe that the following points are very revealing:

- While the major world indexes have hit historic highs, 66% of our portfolio is below the prices reached in 2011.

- While in indexes the companies which have gone up the most are those with the greatest weight, in our portfolios it is just the opposite: we try to give more weight to undervalued companies.

- While indexes trade at high multiples (S&P500 at 26x Shiller’s P/E, and about 20x 2017e), our international portfolio is at 10x profits.

If we compare a representative index, such as S&P500, with our portfolios, we see that we have the BEST companies (greater ROCE) and the CHEAPEST ones (P/E).

| S&P500 | Azvalor Internacional | Azvalor Iberia | |

| ROCE | 15-20% | 39.5% | 20% |

| P/E | 20x | 9.7x | 10.6x |

Thus, it may well be the case, as it happened in 2000, that we witness strong revaluations of our portfolio in the midst of a bear market (remember graph 1). And if there is a fall in stock markets, we believe that our companies will suffer significantly less than the indexes.

With regard to potential opportunities, we are analysing with great interest industries and countries that seem to be forgotten (partly because they are not included in the indexes, but also for other reasons). There are entire sectors trading at low multiples of sunken profits, and although they are, for the most part, bad businesses (capital intensive combining financial and operative leverage) some shares of a higher quality are already reaching the entry price we had set.

As you know, we usually prefer not to go into detail with regard to the specific reasons why we have invested in certain companies. However, we make exceptions in the following two situations:

- When our purchase proved to be a mistake. In this case, we prefer to explain where we went wrong because we believe that transparency increases investors’ confidence. This trust is ESSENTIAL to ensure that our clients avoid selling in times of generalised decline.

- When there is a lot of pessimism in the market (like in 2008). In this case, our experience is that clients appreciate this information, and the risk of competitors taking advantage of our transparency is significantly reduced, since in times of panic nobody has paid much attention to us historically.

However, we will make an exception on this occasion, faced with the barrage of questions from our clients regarding our investment in Google.

Google offers services that are highly valued by their clients (more efficient advertising that traditional media, owing to a very accurate segmentation of the target audience), not requiring much capital and generating a large ROCE of 80%. As advertising in online media weights increasingly more in the mix of total advertising investment (to the detriment of traditional media such as the press), Google still has considerable space to grow: in developed countries, this migration is advanced (yet still ongoing!), but in emerging countries, the potential is huge. For instance, in India, total advertising investment per capita in 2016 reached $6 vs. $600 in the US. This number will increase further with the development of the country, and a significant part will go to online media (the population of India is 4x that of the US).

Next year, its balance sheet will have a net cash position above 10% of Spanish GDP, it is run by its owners, and its accounting is extremely prudent.

The only problem is that the rest of the market already knows all this, and the shares of this type of companies are NOT usually cheap. We took advantage of a moment of scepticism among analysts before the results of the first quarter to buy a block of shares at a multiple below 9x EV/EBITDA, which is only 10% above the historical minimum level of EV/EBITDA reached by the company in 2008. Another way of looking at this is that at our purchase price, Google was worth a little more than double the price of 2007, while its profits since then have multiplied by 9.

Today, Google’s competitive position is very strong given its brand equity, service, scale, network effect and technology. This applies to many fields (Google searches, YouTube videos, Chrome navigation, e-mail via Gmail, mobile operating system via Android, etc.) having a de facto monopoly in some cases.

That being said, the online world is always changing (in fact, just like any other industry!) and we cannot anticipate how the Internet will be used in 20 years’ time, nor if Google will continue to be relevant in its current form. However, we find it reasonable to assume that:

- In 5 years, Alphabet will probably continue to be dominant in its current form (and much larger)

- It will try to adapt (with more or less success) to long-term changes, from a highly advantageous position and a great optionality.

We purchased at levels which suggested an upside potential of 50% and, what is more important, very little downward margin, in our opinion owing to the high cash position (30% of capitalisation) in the balance sheet.

Liquidity

In Azvalor we have maintained a percentage of liquidity between 15%-20% from the start. Our accumulated return of about 20% since inception would have been higher if we had been 100% invested.

However, this “visible” cost of liquidity conceals an “invisible” advantage: the flexibility it gives us to make the most of the opportunities that arise from the many uncertainties surrounding the companies and countries where we invest. We are definitely not original in this sense: managers of the standing of Warren Buffet, Seth Klarman, Tweedy Browne or Southeastern Asset Management (all of them with 4 decades of returns outperforming the market) currently have more liquidity than ever in their portfolios.

An enormous advantage of the investment world is that knowledge builds up, and throughout the years we have studied in great depth many companies that we monitor closely: with little extra work, we are ready to buy new shares as they reach our entry levels. And liquidity is only the option by default when we consider that the safety margin of a stock, whose business we like, is not enough. We will therefore be patient, and wait as long as it takes to put liquidity to work respecting the safety margin that we are comfortable with.

Azvalor news

The result of our work, if we do it well, it to ensure that those who already have money (a little or a lot) have more. We have no objections to this, and it obviously makes us happy; but we would also like to see that people who have nothing can benefit from out work.

After all, the most important things in life (parents’ unconditional love, “standard” health, and in general the Love of others…) we either get them for free or we don’t get them at all, and we would like to give back what we have received “so free”. This is the raison d’être of “DaValor”, the solidarity initiative which continues what we started 10 years ago.

In the past conferences held in Madrid and Barcelona, José María Márquez, its director and old friend, spoke about it for a few minutes, but we would like to follow up this introduction with an event after the summer. Stay tuned because we will soon invite you to join us to better understand and perhaps collaborate with “DaValor”

As this letter draws to a close, we would like to express our gratitude once again for the trust you have placed in our management. The Investor Relations team, led by Beltrán Parages, will be pleased to answer any questions you may have.

Álvaro Guzmán de Lázaro Mateos

CEO and Chief Investment Officer